At the heart of transfer pricing disputes, lies a fundamental question: where is profit actually created?

This is not merely a matter of administrative procedure or numerical calculation, it goes to the core of competing claims over taxing rights among countries.

As multinational enterprises increasingly rely on intangible assets, geographic boundaries become blurred, yet claims over profits grow more aggressive.

In practice, transfer pricing disputes almost usually come down to a single issue: differing interpretations of what constitutes value.

A Classical Debate

Ironically, although the concept of value creation is central to the Base Erosion and Profit Shifting (BEPS) agenda, particularly Actions 8–10, its definition remains open to varying interpretation.

Haslehner and Lamensch (2021) trace the root of this ambiguity to a classic dichotomy:

- Objective value theory holds that value is inherent in the factors of production—namely labor, tangible assets, and manufacturing activities. Under this framework, taxing rights should lie in the place of production.

- Subjective value theory locates value in market perception. Value is no longer determined by the production process, but by how goods or services are valued by consumers. In this view, the market becomes the center of value creation.

The absence of a universal definition exposes a fundamental fragility in the international tax consensus. Two countries may arrive at different conclusions as to where value is created because they do not share a common understanding of what value is.

Today, the objective theory is increasingly overshadowed by the subjective theory, which positions the market as the center of value creation.

From Value Chain to Value Network

The complexity deepens as the economy transitions from a traditionally linear value chain model to a far more fluid value network. Where the location of factories once served as a source of value, that role is now diminishing. Value is increasingly anchored in knowledge and intangible assets.

The challenge is that knowledge does not adhere to clear geographic boundaries. Digital transformation has further complicated—if not impossible—efforts to localize value creation.

This shift fundamentally alters the basis of argumentation in transfer pricing disputes. Countries are no longer competing solely over production activities, but also over claims to innovation, branding, and market access.

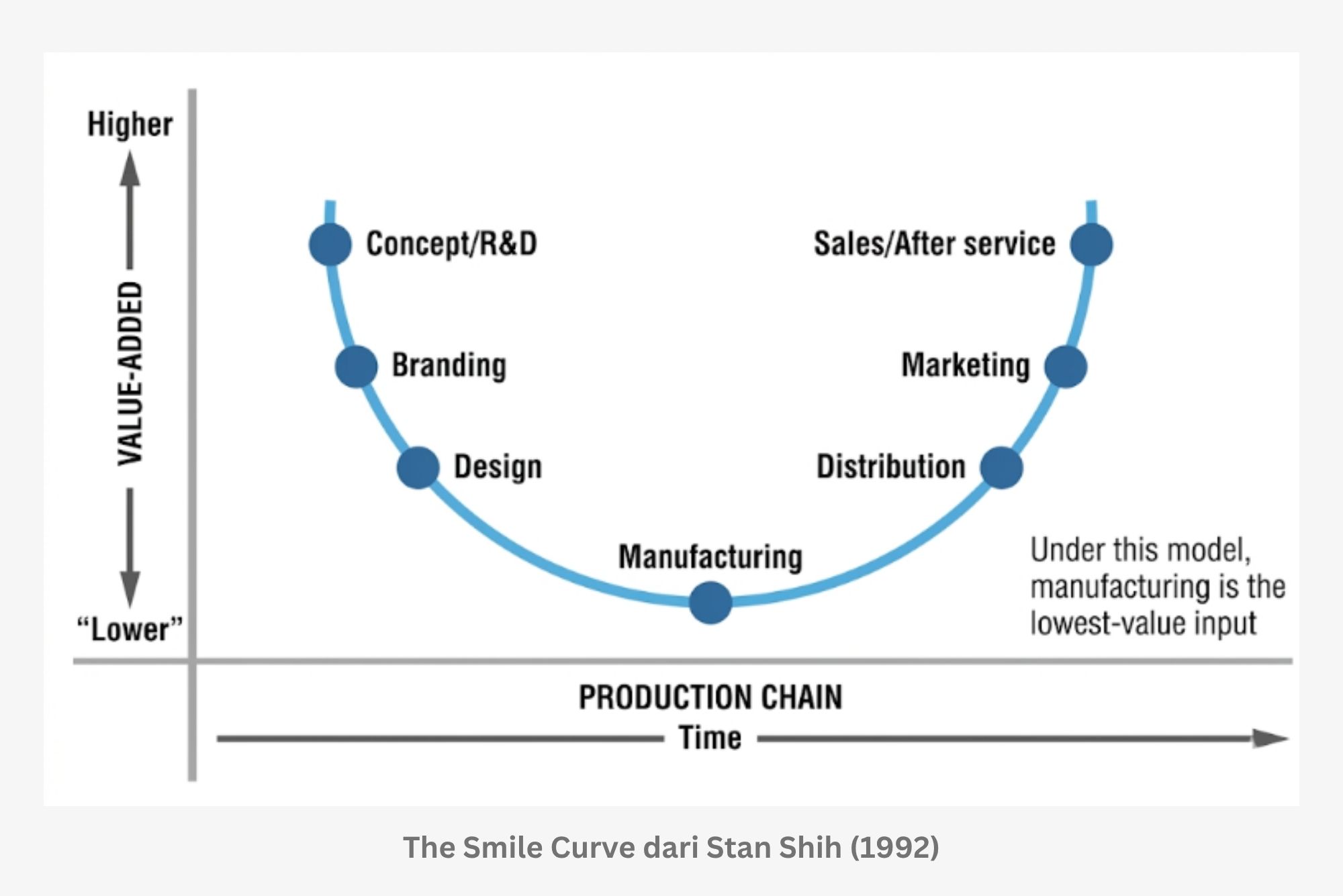

The Smile Curve and Value Imbalance

This phenomenon is clearly illustrated by the Smile Curve, introduced by Stan Shih (1992). The curve demonstrates that economic value is not evenly distributed along the production process; rather, it accumulates at both ends of the spectrum, research and development (R&D) activities (upstream) and marketing and distribution activities (downstream). Meanwhile, physical production lies at the bottom of the curve.

This is where the imbalance lies. Developed countries tend to dominate both ends of the spectrum, whether through ownership of technology or brand power. Developing countries, by contrast, are often confined to the bottom of the curve as production bases with limited value-added. The tangible contributions of production activities in developing countries are reduced to routine functions.

At this point, value is no longer merely an economic concept, but it becomes an instrument in the contest over tax sovereignty.

A Critique of Value Creation

Collier (2021) sharply critiques the concept of value creation as “a concept in search of a principle.” In other words, the doctrine lacks a firm normative foundation comparable to traditional tax law principles.

Although value creation has been incorporated into the BEPS framework, it remains in a formative stage. Although operating as a practical standard, value creation has not fully matured into a settled legal principle.

This raises a critical question: does the adoption of the value creation concept represent an attempt to preserve the relevance of the arm’s length principle in the digital age? Or does it implicitly acknowledge that the existing system has yet to provide a definitive answer to where profits are truly generated?

The Tug-of-War over Tax Sovereignty

Ultimately, the technical complexity of transfer pricing disputes serves as an entry point to a more fundamental issue: the legitimacy of taxing rights. As long as the definition of value continues to favor control over intangible assets rather than physical production activities, this imbalance will persist.

Countries will continue to compete for positions at the “peaks of the Smile Curve,” where economic value is concentrated. Meanwhile, countries that serve primarily as production bases will continue to struggle to defend their taxing rights.

It is here that the issue of tax sovereignty becomes relevant. Value is no longer merely an abstract concept, but a contested arena that determines who has the right to tax in an increasingly borderless global economy. (ASP)

Disclaimer! This article is a personal opinion and does not reflect the policies of the institution where the author works.